Global Vineyard Surface Area

Total area of land planted with grape-bearing vines worldwide

Significance of global vineyard surface area

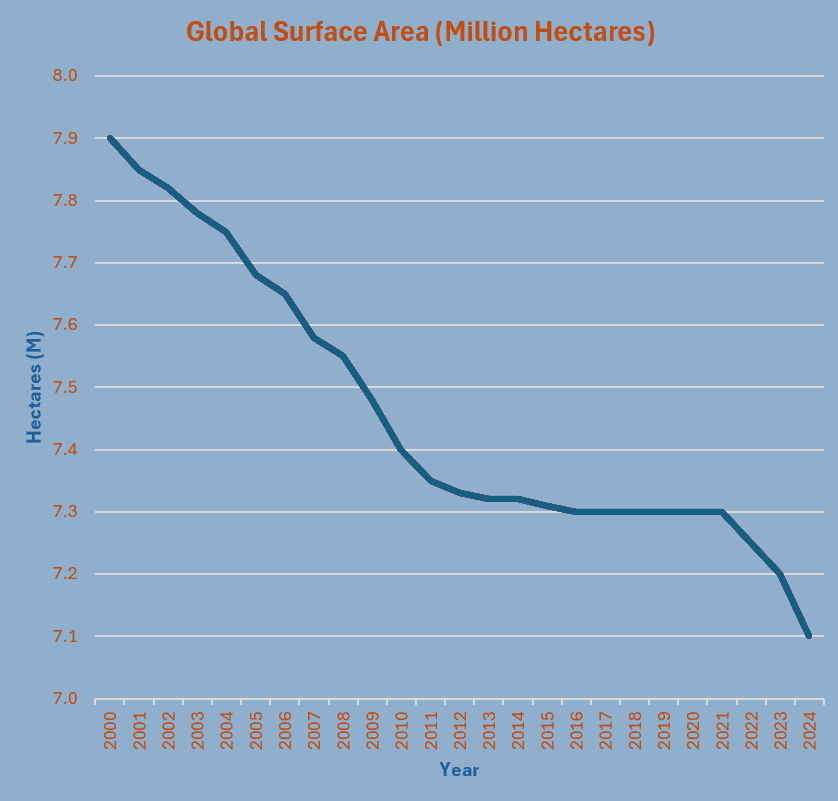

Global vineyard surface area reflects the total area of land dedicated to growing vines for all purposes including wine. The 25 year view shows a decline in vineyard surface area which is leading to a decrease in the production capacity of the wine industry. Production capacity decreases can impact global wine supply, demand and consumer prices. Additionally, the total area of vineyards can provide insights into the health of the wine industry such as industry consolidation, small vs. large vineyard ratio and trends of production costs and quality.

25 Year View

Summary

Global vineyard surface area has declined ~10% since 2000 (from ~7.9 to 7.1 million hectares

2024 compared to 2023, Vineyard Surface Area continued its decline contracting by 0.6% to 7.1 million hectares year over year in major vine-growing regions in both hemispheres. This marks the fourth consecutive year of decline.

The decline / contraction is slow and steady, with a long plateau around 7.3 million hectares from 2010–2021

2024 marks the lowest level in decades, confirmed by OIV, driven by vineyard removals across major regions

Surface Area Decline - Structural drivers:

EU grubbing‑up programs (removal of old vines or vineyards to improve vineyard health, yield or adapt to changing market demands)

Declining wine consumption in Europe

Climate‑driven disease pressure (especially 2023–24)

China’s vineyard contraction

Rising but insufficient growth in India, Brazil, and parts of Latin America

Vineyard Surface Area Map

25 Top Wine Producing Countries

Surface Area Chart

Top 25 Wine Producers

Analysis

Spain, France, Italy, Portugal → long, slow decline/contactions of vineyards

EU grubbing‑up programs

Lower‑value vineyard removal

Climate‑driven disease pressure

Despite shrinking area, value per hectare is rising (premiumization).

China One of the most dramatic vineyard expansions in modern history (2000–2015). Plateau and slight contraction after 2018 due to:

Shifts in domestic demand

Profitability pressures

Table‑grape sector adjustments

USA Stable with slight optimization (380–420 kha)

California dominates

climate stress is shifting plantings northward and to higher altitudes

South Africa Stable to slightly declining.

Water constraints and market pressures shape planting decisions.

Canada Small but steadily growing.

Growth concentrated in Okanagan, Niagara Peninsula and Nova Scotia (fastest‑growing cool‑climate region) .

Latin America (Chile, Argentina) - Mild contraction as producers focus on:

Higher‑altitude sites

Premiumization

Export‑market shifts

Others → absorbs residual to match global totals