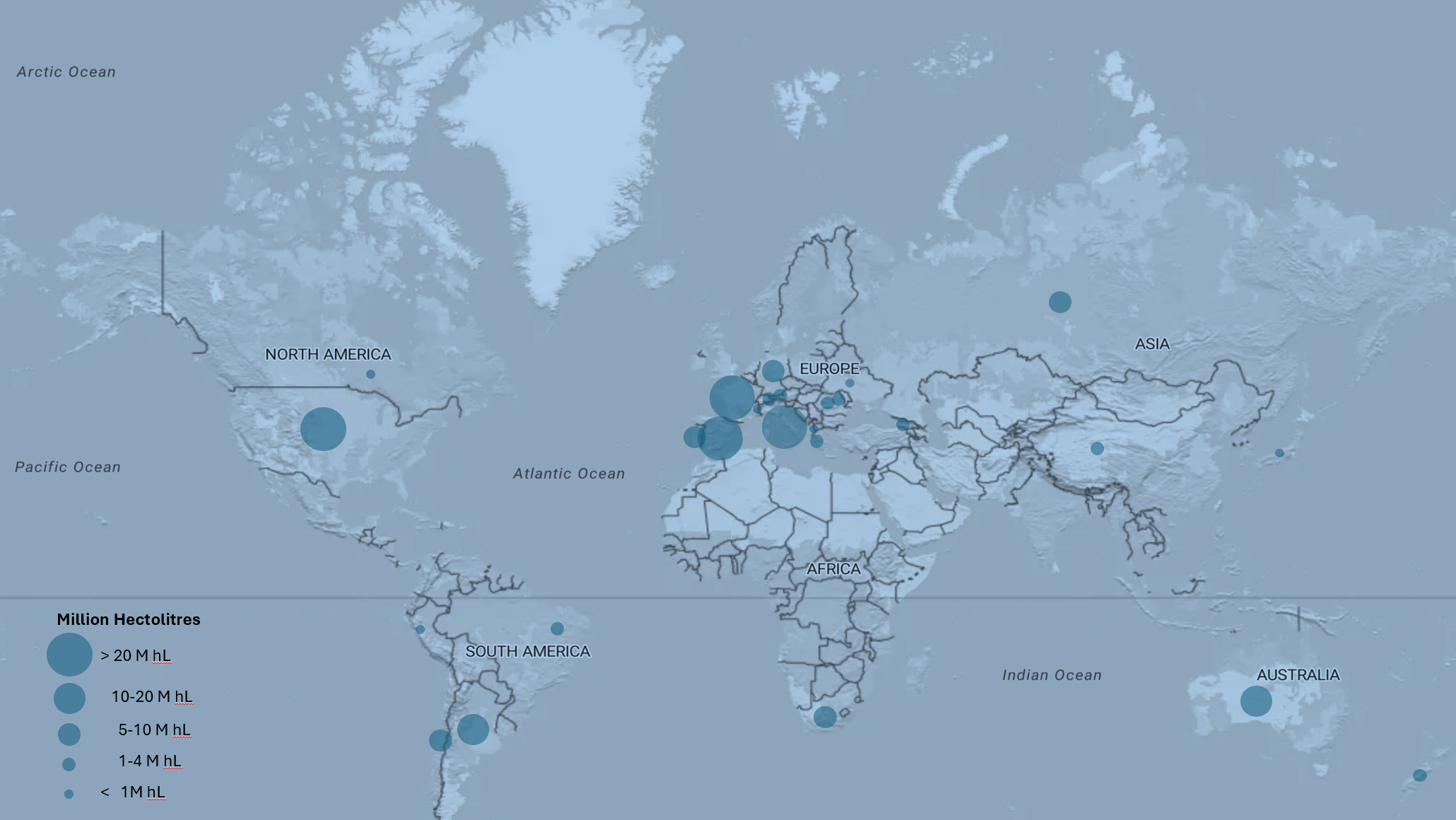

Global Wine Production

Total wine produced worldwide (measured in million hectolitres - mhl)

Significance of Global wine production

Global wine production refers to total volume of wine produced worldwide which is measure in million hectolitres (mhl). Measuring global wine production matters because it reveals the health of the entire wine sector - economically, agriculturally and environmentally. It provides trends and an understanding of how the industry is evolving. It helps producers, importers and policymakers anticipate supply, demand, pricing and trade dynamics.

2024 Global Wine Prod.:

225.85 m hL (million hectolitres)

30.1 billion bottles (standard 750ml bottle)

Top 25 countries:

96% of global wine production

Top 5 Wine Prod. Countries: Italy, France Spain, U.S., Argentina

63% of global wine production

2024 Global Wine Production

Top 25 Countries

Summary

2024 Global Wine Production:

225.85 million hectolitres produced globally in 2024

Equivalent of 30.1 billion bottles of wine (standard 750ml bottle)

Top 25 countries:

96% of wine globally is produced by the top 25 countries

217 million hectolitres or 2.9 billion bottles of wine produced by these top 25 countries

Top 5 Wine Prod. Countries - Italy, France, Spain, U.S., Argentina

Produces 65% of global wine quantity

143.1 million hectolitres or 190 billion bottles of wine produced by the top 5 countries in 2024

Top 25 Countries

Key findings:

Global wine production in 2024 at 225.85 million hectolitres is decreasing continuing a multi-year downward trend and marking the lowest output in more than six decades. This places 2024 well below 2023 levels and the long term average, confirming a sustained contraction in global supply.

2024 production - 225.8 million hectolitres

2023 production - 237 million hectolitres

2024 vs. 2023 - 4.8% net decrease

10 year average - 260 million hectolitres

Change 2024 vs. 10 year average - 13% decrease

Why production is falling globally

Across both hemispheres, the same drivers appear repeatedly:

Extreme climate events (frost, drought, heavy rain, storms)

Disease pressure from humidity and weather variability

Shrinking vineyard area (−0.6% in 2024)

Market‑driven adjustments due to high inventories and lower global consumption

🧭 Regional Highlights

European Union: Lowest output since early 2000s; France saw its lowest since 1957.

Italy: Rebounded slightly from 2023 but still below average.

Southern Hemisphere: Continued low volumes due to climate stress.

🥂 What This Means for the Global Wine Landscape

Supply scarcity is becoming structural, not cyclical.

Producers may shift toward premiumization to offset lower volumes (we can now see this strategy occurring)

Importers (including LCBO‑relevant markets like Ontario) may see tighter allocations and more price pressure in certain categories

Emerging regions (Latin America, parts of Asia) are gaining strategic importance as consumption in these regions is increasing